(Downloads - 0)

For more info about our services contact : help@bestpfe.com

Table of contents

1 Introduction

1.1 Description of problem

1.2 Swedbank

1.3 Background of problem

1.4 Goal

1.5 Purpose

1.6 Limitations

1.7 Approach and Outline

2 Theory

2.1 Options

2.2 Brownian Motion

2.2.1 One dimension

2.2.2 Random Walk Construction

2.2.3 Geometric Brownian motion

2.3 Monte Carlo Simulation

2.3.1 Law of large numbers

2.4 The greek sensitivities

2.4.1 Finite-Difference Approximation

2.4.2 Taylor polynomials

2.5 Interpolation techniques

2.5.1 Linear interpolation

2.5.2 Piecewise Cubic Hermite interpolation

2.6 The Black-Scholes model

2.7 Historical volatility

2.8 Risk free interest rate

3 Method and model implementation

3.1 Methods

3.1.1 Approach 1-3

3.1.2 Approach 4

3.1.3 Approach 5 – Swedbank’s internal estimation model

3.2 Model implementations

3.2.1 Evaluation method

3.2.2 Simulating the Greek sensitivities

3.2.3 Delta-Gamma-Vega Grid – Approach 3

3.2.4 Price Interpolation Grid – Approach 4

3.2.5 Reference points

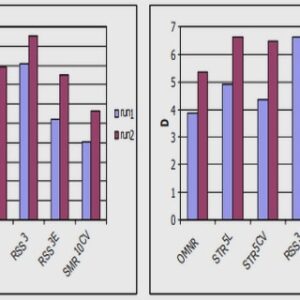

4 Results

4.1 Approach 3

4.2 Approach 4

4.3 Approach 5

4.4 Computational complexity

5 Conclusion

6 Discussion

6.1 Further development

7 References

7.1 Books

7.2 Articles

7.3 Web pages

8 Appendices

8.1 Reference points

8.2 Relative shifts used in Approach 3

8.3 Relative shifts used in Approach 4

8.4 Relative shifts used in Approach 5

8.5 Historical volatility

8.6 Evaluated option

8.7 Approaches versus reference point