Get Complete Project Material File(s) Now! »

CHAPTER 3 LITERATURE REVIEW: ACCOUNTING PRACTICES

INTRODUCTION

The lack of uniformity and acceptable accounting practices in the extractive industries has been recognised over a long period (Luther, 1996:67). Even with the issue of IFRS 6 (IASB, 2010a), Exploration for and evaluation of mineral resources, there are still various accounting interpretations and practices relating to the accounting for exploration and evaluation expenditure.

The aim of this chapter is to investigate the accounting practices of pre-exploration and exploration expenditure by junior exploration companies. The accounting treatment of pre-exploration expenditure in terms of the Framework (IASB, 2010a) and other accounting standards are discussed. The accounting treatment of exploration expenditure is included in the scope of IFRS 6 (IASB, 2010a); therefore the main features of IFRS 6 (IASB, 2010a) are investigated in this chapter. The layout of this chapter is as follows

PHASES OF MINING

There are various phases of mining, but junior exploration companies are only involved in the pre-exploration and exploration phase. Table 3.1 illustrates the different phases of mining.

The pre-exploration phase refers to all expenditure incurred before an entity has obtained the legal right to explore a specific area, therefore all expenditure incurred by a junior exploration company before a prospecting right is obtained classifies as pre-exploration expenditure. The exploration phase begins when the prospecting right is obtained and ends upon completion of a feasibility study (KPMG, 2009). The mine construction phase generally begins after completion of a feasibility study and ends upon the commencement of production (KPMG, 2009). The operation phase commences with the production of minerals from the mining of the mineral reserves. The closure phase commences with the termination of production and includes activities such as decommissioning and dismantling equipment, restoring the mine site as a result of damage caused to the environment during the development of a mine and from ongoing mining activities, and ongoing care and maintenance of closed mines (KPMG, 2009).

IFRS 6 (IASB, 2010a) deals specifically with the expenditure relating to the exploration phase. The recognition and measurement of pre-exploration expenditure are discussed in section 3.6 while the requirements of IFRS 6 (IASB, 2010a) on exploration and evaluation expenditure is discussed in section 3.7. The construction, operation and closure phases of mining are not dealt with in IFRS 6 (IASB, 2010a) and, thus, mining companies shall apply the Framework (IASB, 2010a), other IFRSs (IASB, 2010a) and IASs (IASB, 2010a) issued by the IASB to transactions, assets and liabilities incurred during these latter phases.

MINERAL ASSETS OF EXPLORATION COMPANIES

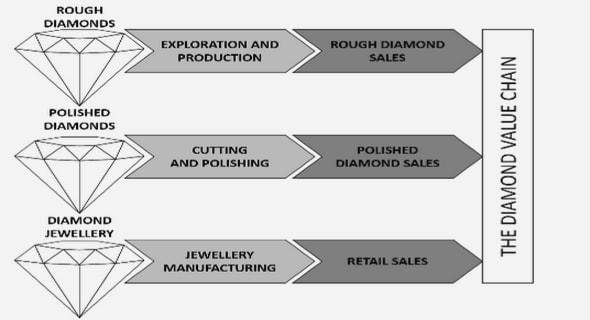

Before the accounting practices of junior exploration companies are discussed it is important to understand the underlying asset that is created by doing exploration activities. As per the presentation by Davel (2009), the main asset of mining companies initially comprises the legal rights to explore an area with these exploration activities then resulting in knowledge and, ultimately, mineral reserves being identified. Accordingly, the main asset of junior exploration companies are the prospecting rights that will develop from the knowledge that were obtained from surveys, boreholes, trenches, pits and other prospecting work about the mineral reserves and resources into the production of mineral reserves. The results obtained from the exploration phase will indicate whether the mineral resources are inferred, indicated or measured and it is from these results that a company will be able to classify the mineral reserve as either probable or proven.

The Souh African Code for the Reporting of Mineral Asset Valuation (SAMVAL Code) (SAMCODE, 2008) sets out minimum standards and guidelines for the public reporting of mineral asset valuations in South Africa. This code was drawn up under the joint auspices of the Southern African Institute of Mining and Metallurgy (SAIMM) and the Geological Society of South Africa (GSSA). According to the SAMVAL code (SAMCODE, 2008) the term “mineral resources” may be defined as

A concentration or occurrence of material of economic interest in or on the earth’s crust in such form, quality and quantity that there are reasonable and realistic prospects for eventual economic extraction. The location, quantity, grade, continuity and other geological characteristics of a mineral resource are known, or estimated from specific evidence, sampling and knowledge interpreted from an appropriately constrained and portrayed geological model. Mineral resources are subdivided, and must be so reported, in order of increasing confidence in respect of geoscientific evidence, into inferred, indicated and measured categories (SAMCODE, 2008).

According to paragraph 22 of the South African Code for the Reporting of Exploration Results, Mineral Resources and Mineral Reserve (SAMREC Code) (SAMCODE, 2007) the term “inferred mineral resources” is defined as “… that part of a mineral resource for which volume or tonnage, grade and mineral content can be estimated with only a low level of confidence…”. An inferred mineral resource is characterised by the lowest level of confidence.

Paragraph 24 of the SAMREC Code (SAMCODE, 2007) defines indicated mineral resources as “… that part of a mineral resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a reasonable level of confidence …”. Indicated mineral resources have a higher level of confidence than inferred mineral resources but a lower level of confidence than measured mineral resources.

Paragraph 25 of the SAMREC Code (SAMCODE, 2007) defines measured mineral resources as “… that part of a mineral resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a high level of confidence…”. Measured mineral resources indicate the highest level of confidence.

According to the SAMVAL Code (SAMCODE, 2008) the term “mineral reserves” may be defined as The economically mineable material derived from a measured or indicated mineral resource or both. It includes diluting materials and allows for losses that are expected to occur when the material is mined. Appropriate assessments to a minimum of a Pre-Feasibility Study for a project, or a Life of Mine Plan for an operation, must have been carried out, including consideration of, and modification by, realistically assumed mining, metallurgical, economic marketing, legal environmental, social and governmental factors. Where the term ‘ore reserve’ is used, this is synonymous with the term “mineral reserve”.

A reserve refers to the economically mineable material in the mineral resource. Paragraph 33 of the SAMREC Code (SAMCODE, 2007) defines a probable mineral reserve as “… the economically mineable material derived from a measured or indicated mineral resource or both. It is estimated with a lower level of confidence than a proved mineral reserve …” while paragraph 34 of the SAMREC Code (SAMCODE, 2007) defines proved mineral reserve as “… the economically mineable material derived from a measured mineral resource. It is estimated with a high level of confidence …”. Thus, according to the SAMREC Code, when a mineral reserve is classified as a proven mineral reserve such a mineral reserve represents the highest level of confidence obtainable. Figure 3.1 illustrates the relationship between the exploration results, mineral resources and mineral reserves.

According to paragraph 21 of the SAMVAL Code (SAMCODE, 2008), the three generally accepted approaches to mineral asset valuation include the cash flow approach, market approach and the cost approach. Paragraph 21 of the SAMVAL Code (SAMCODE, 2008) defines these approaches as follows:

- The Cash Flow Approach relies on the ‘value-in-use’ principle and requires a determination of the present value of future cash flows over the useful life of the Mineral Asset.

- The Market Approach relies on the principle of ‘willing buyer, willing seller’ and requires that the amount obtainable from the sale of the Mineral Asset is determined as if an arm’s-length transaction had occurred.

- The Cost Approach relies on historical and/or future amounts spent or to be spent on the Mineral Asset

Both the cash flow and the market approaches use various estimates and assumptions in order to value mineral assets.

As discussed above, the main asset of an exploration company evolves over time and, ultimately, the exploration activities will confirm probable and/or proved mineral reserves. In addition, as discussed in section 3.5.3, after recognition, exploration and evaluation assets may be measured using either the cost model or the revaluation model. The revaluation model depends on the classification of the assets.

As per the presentation by Davel (2009), although the cost model is verifiable, it has limited relevance to the users of financial statements, as there is no connection between the historical exploration costs incurred and the future cash flows that will be generated from the mining property. The cost model is also cost effective and not time consuming. In order to obtain the fair value of the main asset of the exploration company various subjective assumptions and estimates are required. As per the discussion above, various assumptions are used both to classify and to value mineral resources and reserves. It would, however, take both time and effort to carry out these valuations and the process would require input from various professional people. Exploration companies would have to consider the cost of obtaining these values and whether these values would be meaningful to the users of the financial statements.

As discussed in section 3.5.6 the disclosure requirements of IFRS 6 (IASB, 2010a) are limited. Accordingly, a comprehensive disclosure of the main assets of exploration companies is important as this will enable the users of the financial statements to make their own assumptions and estimates about the value of the underlying main asset of exploration companies.

HISTORICAL OVERVIEW OF THE FUNDAMENTAL ACCOUNTING METHODS USED IN THE SOUTH AFRICAN MINING SECTOR

Before the promulgation of the MPRDA, Jourdan (cited in Cawood & Minnitt, 1998:373) was of the opinion that the large mining houses held almost all mineral rights. As a result, these mining houses carried out almost all exploration activities in South Africa. To provide background information of the previous accounting practices that influenced the accounting for exploration and evaluation expenditure are discussed. The South African Institute of Chartered Accountants (SAICA) issued a guideline on the accounting and reporting practices in the mining industry (SAICA, 1995). This methodology contained in the guideline is based on the basic principle that mines have a finite life (SAICA, 1995:1). When all the mineral reserves have been extracted from a specific area the company will close down and, therefore, mineral reserves may be regarded as a “wasting asset” (Luther, 1996:68). The guideline prescribed the accounting methodology called the “appropriation method” (Davel, 2005). “This methodology simulates cash flow accounting and is based on the argument that mines have a finite life and that the retention of funds to replace the mining facility is pointless” (Davel, 2005). For this reason, capital expenditure is regarded as irretrievable and no depreciation is provided (Luther, 1996:79). The appropriation method was more commonly used than any other method and has the same result as when all capital expenditure is expensed (SAICA, 1995:1). Accordingly, all pre-exploration and exploration expenditure incurred was immediately expensed in the financial statements.

Another method used by various mining companies was the “amortisation method” (SAICA, 1995:1). This method intended to match costs and revenues by the amortisation of the capitalised cost of mining assets, which included the costs of exploration and evaluation, infrastructure, development costs, pre-production costs and capitalised interest, over the estimated life of the mining operation (SAICA, 1995:3). This method was regarded as appropriate for mining companies that were likely to continue mining or exploiting new mineral resources over an extended period of time (SAICA, 1995:3).

CHAPTER 1.INTRODUCTION.

1.1.BACKGROUND TO THE STUDY

1.2.PRELIMINARY LITERATURE STUDY

1.3.RESEARCH QUESTION AND HYPOTHESIS

1.4.RESEARCH OBJECTIVE.

1.5.RESEARCH METHODOLOGY

1.6.WHO COULD BENEFIT FROM THE STUDY?

1.7.LIMITATIONS OF THE STUDY.

1.8.LIST OF DEFINITIONS USED

1.9.LIST OF ABBREVIATIONS AND ACRONYMS USED

1.10.OUTLINE OF CHAPTERS

CHAPTER 2.LITERATURE REVIEW: HISTORICAL OVERVIEW OF MINERAL RIGHTS IN SOUTH AFRICA

2.1.INTRODUCTION

2.2.MINERAL LAW IN SOUTH AFRICA

2.3.SUMMARY AND CONCLUSION

CHAPTER 3LITERATURE REVIEW: ACCOUNTING PRACTICES.

3.1.INTRODUCTION..

3.2.PHASES OF MINING

3.3.MINERAL ASSETS OF EXPLORATION COMPANIES.

3.4.HISTORICAL OVERVIEW OF THE FUNDAMENTAL ACCOUNTING METHODS USED IN THE SOUTH AFRICAN MINING SECTOR1

3.5.OVERVIEW OF IFRS

3.6.PRE-EXPLORATION EXPENDITURE .

3.7.EXPLORATION AND EVALUATION EXPENDITURE

3.8 NEW DEVELOPMENTS

3.9.SUMMARY AND CONCLUSION.

CHAPTER 4LITERATURE REVIEW: TAXATION PRACTICES

4.1.INTRODUCTION

4.2.HISTORICAL OVERVIEW OF MINE TAXATION IN SOUTH AFRICA.

4.3.APPLICATION OF THE INCOME TAX ACT TO EXPLORATION COMPANIES

4.4.VENTURE CAPITAL

4.5.SUMMARY AND CONCLUSION

CHAPTER 5.RESEARCH METHODOLOGY

5.1INTRODUCTION

5.2LITERATURE REVIEW

5.3LIMITATIONS OF THE LITERATURE REVIEW

5.4THE POPULATION.

5.5THE SAMPLE

5.6DATA COLLECTION METHOD.

5.7THE QUESTIONNAIRE

5.8DATA ANALYSIS .

5.9LIMITATIONS OF THE EMPIRICAL INVESTIGATION.

5.10SUMMARY AND CONCLUSION

CHAPTER 6RESEARCH RESULTS.

INTRODUCTION

6.2THE QUESTIONNAIRE

6.3RESEARCH RESULTS

6.4SUMMARY AND CONCLUSION..

CHAPTER 7CONCLUSIONS AND RECOMMENDATIONS

7.1INTRODUCTION

7.2RESEARCH QUESTION AND HYPOTHESIS.

7.3RESEARCH OBJECTIVE

7.4RESEARCH FINDINGS

7.5SUMMARY AND CONCLUSION

7.6RECOMMENDATIONS

7.7CONTRIBUTIONS OF THIS STUDY TO THE ACCOUNTING SCIENCES

BIBLIOGRAPHY

GET THE COMPLETE PROJECT

ACCOUNTING AND TAXATION PRACTICES OF SELECTED MINING EXPLORATION COMPANIES IN SOUTH AFRICA